As an investor at Inovia, I work with a team that has over 15 years of experience partnering with exceptional healthcare companies like AlayaCare, BenchSci, Vital, Signal1 and Forward. While I’ve spent the last three years meeting with many healthcare startups, I have a deeper expertise in Customer Experience solutions. My prior life was spent in “horizontal” B2B SaaS, where I got the chance to see how Salesforce, one of the very first B2B SaaS companies out there, grew from a revolutionary sales tool into a full-suite enterprise platform helping organizations of all sizes manage and enhance customer relationships.

Over these past years as an investor, I’ve gotten to understand the many nuances and obstacles healthcare founders must navigate in the industry. From misaligned incentives (between payers, providers, and regulators) to slow software adoption (doctors still use software from the 70s) to regulatory capture benefiting certain tech vendors to the detriment of younger upstarts, the list of healthcare pitfalls goes on. Despite the many differences, I noticed some parallels between the world of horizontal B2B SaaS (especially customer success or CX software tools) and healthcare software platforms, and I found some learnings from the CX world that might be relevant for healthcare companies.

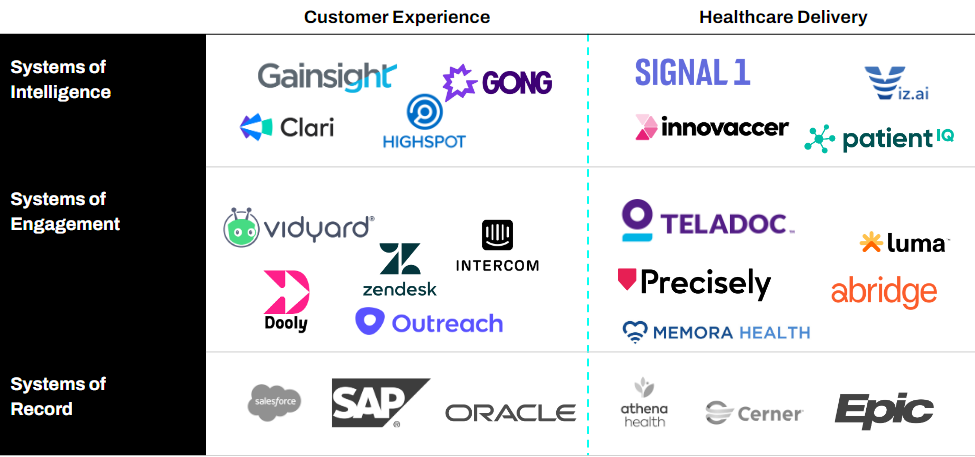

In the CX world, everything revolves around the customer, and CRMs (customer relationship management software) are the systems of record which maintain all critical customer data. Following the adoption of these foundational platforms, we’ve seen the proliferation of customer engagement solutions (e.g. chat interfaces and sales outreach sequencing) and intelligence layers (e.g. customer interaction suggestions and predictive analytics). We saw a similar evolution in the healthcare software world: Electronic Health Records (EHRs) have reached near total market adoption (95% of clinics/hospitals have an EHR) and are the key repositories of patient data. Over the past few years, we have had the chance to meet with an exciting crop of healthcare startups building new enablement and engagement solutions. Based on our learnings from the CX space, we believe there is potential to build massive companies at the engagement and intelligence layer in healthcare. Still, we remain mindful of the rebundling and consolidation that has been taking place in the sales and service space.

Overview of parallels between CX platforms and healthcare platforms

Systems of Record

In both the world of CRMs and EHRs, a handful of platforms dominate the market (Salesforce/SAP/Oracle vs Epic/Cerner/Athena), although I would note that the EHR market has a much longer tail of smaller vendors (800+), partially spurred by government incentives over a decade ago (e.g. the HITECH act). These large CRM and EHR vendors have been around for some time; they are worth hundreds of billions and have built large platforms across a gamut of use cases. When we compare these mega-players, a few differences do stand out, especially when it comes to fostering a healthy third party ecosystem: Salesforce has been a pioneer of the AppExchange strategy since 2006, while Epic, having launched its App Orchard in 2016, has been notably more cagey in its collaboration with third-party software vendors. We can also see this in the M&A patterns of the companies, with Salesforce frequently acquiring and integrating companies into its platform (Slack, Tableau, and Mulesoft, to name a few), whereas Epic has not pursued any meaningful M&A. That being said, there seems to be some positive momentum on the marketplace front, with Epic relaunching its third party marketplace this year, and we will be keenly tracking how this will impact digital health startups.

In healthcare, we see the opportunity to build systems of record in multiple sub-sectors. Even though healthcare is a multi-trillion market, it is composed of many sub-verticals where we see the opportunity to build significant healthcare platform companies. Companies like Elation and Canvas are building next-generation EHRs tailored specifically to primary care providers and value-based care systems. Other players like Medfar have been rolling up the long tail of EHRs. We also see large opportunities in verticalized clinic software, like fertility, dermatology, and mental health, not to mention the pharma/clinical trial space, with companies like Medable emerging as full-stack platforms managing the clinical trial process from end to end.

Systems of Engagement

In the CX world, systems of engagement help companies design the optimal paths for customer interaction. For example, companies like Vidyard and Loom pioneered video-based customer messaging, while Outreach and Salesloft established email sequencing and cadences to increase sales rep productivity and convert more deals in the pipeline. In the same way, digital health platforms have emerged to better engage with patients, optimizing the right channel for care delivery and communication/follow-ups. Companies like Teladoc and Dialogue paved the way for delivering telehealth at scale, while Luma, Precisely, and Memora Health are helping optimize care navigation, appointment scheduling, care plans, follow-ups and more. Another component of engagement platforms is saving time: the age-old adage in sales is that reps spend over half of their time on non-sales activities. Note-taking apps like Dooly free up sales reps’ schedules by automating/speeding up data capture and recording it in the CRM. In the same way, we are seeing companies like Abridge and DeepScribe help reduce physician burnout by automatically capturing patient interaction notes.

Patients expect more from their healthcare providers, which will drive the success of systems of engagement in the healthcare world. Increasingly, there is a disconnect between how patients receive healthcare services and how they experience many other spheres of their lives (seamless banking apps, same-day e-commerce deliveries, personalized music/TV recommendations). The “consumerization of healthcare” gives room for digital health companies to help providers fill the needs of patients looking for more personalized and timely communication channels and care delivery that fits their needs.

Systems of Intelligence

In both industries, having a single view of the customer (or patient) is paramount to providing a high-quality service. With multiple stakeholders (doctors, nurses, pharmacists and sales reps, solution engineers, and customer success managers) interacting with the same individual, it is difficult to keep track of every piece of information and interaction. In the customer experience world, systems of intelligence help companies analyze customer data, identify patterns and anticipate needs, boosting customer satisfaction and resulting in more tailored messaging and offerings. Companies like Gong and Chorus analyze customer interactions and coach reps by leveraging AI to serve their clients better. Gainsight is a customer success platform that helps identify each customer’s “health” (no pun intended), determining which are at risk or churning and which ones have a propensity for upselling. In the healthcare world, systems of intelligence have an even larger potential to transform care delivery by empowering providers with data on their patients, unlocking predictive signals and guiding them toward the best method of care. Signal1 provides hospitals with real-time insights, such as which patients are ready for discharge and identifying patients with a high burden of care. Innovacer and PatientIQ are collecting a trove of patient data, including disease status, visit types, procedure codes and more, to monitor patient progress and predict patient outcomes.

Health data interoperability will make healthcare systems of intelligence even more powerful. In the customer experience world, companies strive to have a comprehensive view of their customers via their own customer touchpoint channels (sales, service, marketing), but they will more rarely share this information with other partners or competitors. In addition, privacy laws are increasingly protecting customers’ information, making external customer data gathering more challenging. On the flip side, health data is becoming increasingly open (while respecting patients’ privacy), with providers increasingly sharing information to promote transparency and continuity of care. The rise of value based care payments in the US should incentivize providers to deliver better care, leading them to look for a full picture of population data rather than tracking procedures and transactions (which is what original EHRs were focused on). We also expect a future where patients have increased access to their own health data and can make more informed decisions about how they receive care, enabling healthcare companies and providers to provide better services.

Key Lesson: The Great Re-Bundling of Software

An evolution that we’ve observed with CX software companies is the potential to move beyond point solutions to full platforms. As some like to say, “You either die a point solution or live long enough to see yourself become a platform.” We recently saw a category of “Alpha platforms” build a portfolio of adjacent solutions, like Zoominfo going from sales lead intelligence to sales call analysis (via Chorus acquisition), and Gong, which has been encroaching in Outreach’s territory by launching a sales engagement offering to help reps with customer outreach and communication.

Customers in healthcare are also increasingly looking for bundled platforms vs point solutions. We heard from one health insurer looking to simplify the number of vendors they work with as they have too many disparate sources of information. They recommend digital health companies focus on articulating a solid data integration strategy when pitching to customers.

We are seeing a promising crop of companies carving out a platform play in healthcare, like Viz.ai which has been able to break out from purely being an AI diagnostics platform to becoming a full-fledged care coordination platform. BenchSci in our portfolio has also evolved from its initial Antibody and Reagent Selector products that targeted a very important but specific challenge in the pre-clinical process towards its full-suite ASCEND platform that accelerates the drug discovery process across the entire lifecycle. We are extremely excited to find the next-generation software companies that will drive better health outcomes while building successful companies and platforms. Whether you’re a founder, an operator or an investor, if you’re just as excited as we are about healthcare systems of record, engagement, and intelligence, we would love to chat!