Welcome to Beyond the Cart. Over the course of this blog series, I will be sharing insights and thoughts on the latest trends and technologies that are driving the e-commerce industry forward. I’ll look at a wide range of topics, from perspectives on commerce enablement and thesis areas Inovia has developed around them, to my thoughts on tech-enabled business models and where we believe the future of the e-commerce ecosystem is headed. I’m excited to share my perspectives with entrepreneurs, investors, and anyone else passionate about the future of e-commerce!

A lot has happened in e-commerce over the past two years and there has been much speculation over what the future of online purchasing might look like. Of all the predictions made, the most headline-grabbing was around the idea that brick-and-mortar would become extinct with a new wave of e-commerce, where shoppers default to the convenience of online shopping. As it turns out, many of these predictions missed the mark. Having backed e-commerce and omnichannel software platforms for the last decade, Inovia is well positioned to understand the dynamics at play and identify emerging opportunities in the industry.

We believe the future of e-commerce revolves around commerce enablement (the VC e-commerce buzzword of the day). To define and simplify commerce enablement, we think about it as the process of digitizing spend through online channels. Commerce enablement therefore presents an opportunity to increase the data it collects on customers to grow revenue and on internal operations to drive efficiencies.

______________________

Commerce Enablement Stack

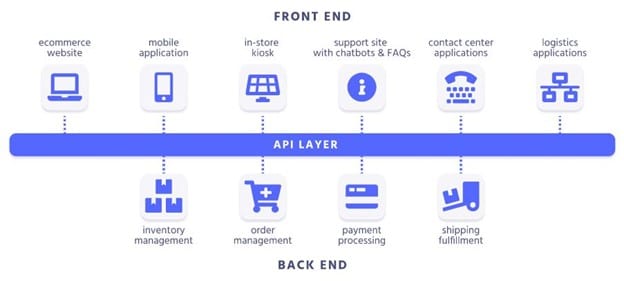

Though commerce enablement technically covers the entire value chain, the way we see the evolution of commerce enablement at the software level is across three different layers:

Platforms

E-commerce platforms are adapting to the market pull for a best-of-breed approach by offering out-of-the-box solutions from day one and with the comfort of swapping different components for third-party apps. This strategic shift can be seen with the development of first-party apps that can be seamlessly integrated and deployed. The result is accelerated time to value for an e-commerce platform which enables merchants to preserve optionality in their tech stack over the long-term. Fabric is pioneering the headless-first approach to creating a first-party app ecosystem around their platform with pre-built integrations into market leading third-party apps. Shopify has taken a similar stance with Shopify Editions, announcing 100+ first-party apps, to create an out-of-the-box Shopify platform.

Middleware

Middleware is evolving to facilitate best-of-breed e-commerce. Merchants can now assemble a platform-agnostic e-commerce stack, creating an open ecosystem for e-commerce software by overcoming the engineering constraints of integration that previously made this approach incredibly challenging (eg. data standardization, platform integrations, etc.). Though nascent, we expect more challengers to emerge over time as the middleware category will play a significant role in commerce enablement. Rutter is a trailblazer in the middleware category with its universal commerce API, which allows merchants to connect to almost any e-commerce platform with a single line of code, enabling them to sync orders from multiple sources instantly.

Applications

The combination of an open ecosystem approach from e-commerce platforms and robust middleware is a massive tailwind for the application layer. Apps can now diversify their revenue streams across e-commerce platforms. There is a new competitive dynamic with first-party apps within each respective ecosystem (eg. Fabric, Shopify) but entire product categories are now up for grabs and we are seeing accelerated value creation.

- Established Category Killers: Our view is the future of commerce enablement will be a best-of-breed approach, as winners emerge in their respective app verticals. Some examples include Klaviyo (email marketing), Attentive (SMS marketing), and Chargebee (subscriptions), to name a few.

- Emerging Category Killers: Some up-and-coming players that we believe are on the cusp of becoming a category killer are Tapcart (no-code mobile app development), Gorgias (customer support), and Loop Returns (returns & exchanges).

- App Platforms: Some players are taking a platform approach by rolling up value chain segments to offer a packaged app offering, such as Yotpo (marketing, reviews, loyalty). We believe e-commerce apps will get rolled up over the next few years and we expect to see some consolidation in the space, but the jury is out on whether the app platform approach will be successful in the long term (particularly due to middleware as the wildcard enabling best-of-breed).

______________________

Commerce Enablement by Segment

Our envisioned future for commerce enablement bifurcates by merchant scale between SMB & Midmarket and Enterprise.

Delivering ROI to the Long Tail of SMB & Midmarket Merchants

As we all know, SMB & Midmarket merchants have simpler needs than Enterprise, making the ROI calculation of incremental spend on an e-commerce stack more challenging. The long tail of merchants want a turnkey platform and easy deployment which is how Shopify initially made its killing. However, there were scaling challenges for merchants who wanted more flexibility with their e-commerce stack.

Initially, the emerging trend was going headless, meaning separating the front-end shopping interface from the back-end meat and potatoes of an e-commerce platform. The benefit being more control over the digital shopping experience with more customizable UX/UI. We’ve observed a trend where merchants are reverting back from headless front-ends because the ROI calculation makes it hard to justify; the revenue lift of going headless with an enhanced front-end is not enough to offset ongoing maintenance costs.

Another trend we’ve noted is the movement towards microservices-based architecture that enables tech stacks to conform to merchants’ needs (Fabric illustrates the transition from monolith to microservices beautifully here). I like to simplify this by thinking of each function/application in the e-commerce stack as a lego block with a 1-click integration; merchants can assemble their stack a-la-carte with the flexibility to make substitutions on the fly. The outcome is a best-of-breed approach, meaning you can pick the best app for you, which is where category killers at the app layer were born.

From Inovia’s point of view, a key catalyst to commerce enablement for SMB & Midmarket will be middleware because it allows merchants to be platform agnostic. The foundational layer of an e-commerce store will dwindle in importance as piecewise solutions can be woven together.

Bringing Best-of-Breed to Enterprise

Although digitally native e-commerce brands have demonstrated proof-of-concept for a lot of commerce enablement tools and products, our view is that Enterprise will drive the future of commerce enablement because that’s ultimately where the money is.

There was formerly a chicken and egg problem with commerce enablement that created a lag in e-commerce adoption for the Enterprise segment: you needed to have the right platform architecture to plug-in to other programs/apps, but you also needed a rich ecosystem of programs/apps to be plugged-in to. System architecture was a big roadblock because platforms were Frankensteined together with custom integrations that required a heavy engineering lift (often via an expensive system integrator). Replatforming was time consuming and expensive, while also creating a high total cost of ownership problem because many APIs had load-based pricing schemes that were unfeasible at scale (ie. high volume = high costs).

E-commerce platforms are evolving to accommodate Enterprise needs with robust API integration with palatable total cost of ownership. The middleware layer is less applicable due to the customization required for many legacy stacks; we believe that will continue to change over time as today’s Midmarket merchants, utilizing modern stacks, grow to Enterprise in the future. The ability to plug-and-play with microservices will be crucial to optimize ROI on the tech stack with a best-of-breed approach.

We have observed that best-of-breed solutions increasingly include omnichannel B2B marketplaces across merchant segments, which we believe to be an important pillar for the future of commerce enablement.

The Rise Of Omnichannel B2B Marketplaces

Something that excites us most about the infrastructure level is the proliferation of omnichannel B2B marketplaces. Merchants have massive B2B spend behind the scenes where a lot of incremental value can be unlocked by an e-commerce solution to enable an omnichannel approach.

B2B e-commerce adoption lags B2C by several years because merchant requirements are complicated, often requiring some degree of customization (eg. products, catalogs, data, etc.). As such, B2B commerce is still largely underpenetrated. Legacy click-price-quote ordering systems with traditional sales rep channels remain prevalent; this presents a massive opportunity for e-commerce platforms offering a modern omnichannel approach to deliver an Amazon-like experience with low friction.

We believe API-first marketplaces with B2B modules have a huge potential to disrupt traditional channels. Merchants will maintain control of the UX/UI of the platform while seamlessly integrating into back-end e-commerce platforms. By leveraging a centralized strategy for D2C and B2B e-commerce, there is ample opportunity to drive ROI:

- A simplified IT stack with a streamlined back-end reduces the ongoing engineering burden of maintaining several platforms

- Increased visibility leads to better decision-making at the operational level (eg. inventory management, supply chain, logistics, etc.)

- More competitive pricing on material inputs and tail spend

Some examples of the most exciting B2B marketplaces that Inovia has engaged with include:

- Nautical Commerce: Democratizing access to multi-vendor marketplace technology, supporting D2C and B2B channels

- Convictional: Supplier enablement software enabling retailers to connect with their dropship, marketplace, and wholesale suppliers

- Spryker: Omnichannel e-commerce platform doubling down on solving sophisticated B2B commerce to accelerate digital transformation at the Enterprise level

That’s it for episode one of Beyond the Cart! We hope you enjoyed Inovia’s views on commerce enablement. Please see our website to read more about our commerce portfolio companies.

Stay tuned for part two!